Suburb record: 24 Starritt Place, Macarthur. Photo: LJ Hooker Tuggeranong.

Momentum is building in Canberra’s detached house market with prices rising again in October, fuelled by the Commonwealth 5 per cent deposit scheme for first-home buyers.

Cotality’s latest Home Value Index for October shows house prices up a further 0.7 per cent, taking the year’s increase to 3.6 per cent, and 3.4 per cent for the last 12 months.

In contrast, unit and townhouse prices remain stagnant, with hardly any movement over the month, registering a 0.1 per cent blip.

This is the year they have only risen 0.3 per cent, with annual results flat, reflecting the good supply of stock in the market.

However, the combination of new buyers in the sub-million-dollar range and a limited number of properties is driving up house prices.

Across all property types, Canberra prices rose 0.6 per cent.

The annual price growth figures show a clear north-south divide

Growing Molonglo remains the leader at 6.8 per cent, with its new stock, but Tuggeranong is now second at 4.7 per cent, followed by Weston Creek (4.4%) and a resurgent blue-ribbon South Canberra (4.3%).

North Canberra remains in the doldrums at 0.9 per cent, followed by Gungahlin (2.1%) and then Belconnen (3.6%).

Agents report busy open homes in Tuggeranong with buyers seeing value in the Valley’s standalone family houses.

A Macarthur home set a suburb record of $1,755,000. The four-bedroom, three-bathroom house with three living areas and an outdoor entertainment area and pool had been held by the same family since it was built in 1991.

The Property Collective’s Will Honey said there had been increased buyer activity in October, particularly in the under $1m range, and much of that was in Tuggeranong.

“That million dollars property price range is getting lots of interest,” he said. “We’ve had a really busy October.

“The first indicator is the numbers of visitors through open homes and we’re seeing an uptick this spring for sure, and it’s in that lower sort of price range.

“There are still properties moving above that but most of the activity is in that range.”

The unit market was moving more slowly but it depended where you were. Mr Honey said the established apartment market was still considerably cheaper than the new market, so that was driving a lot of the sales.

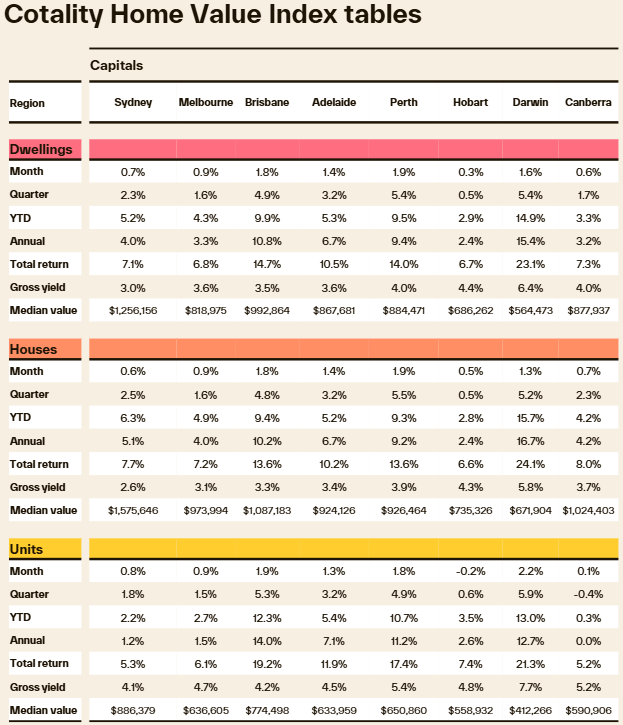

Cotality Home Index Value November 2025. Table: Cotality.

Cotality research director Tim Lawless said the price growth in Tuggeranong and Molonglo was quite a bit stronger than the broader average for Canberra.

“You have to point towards the affordability of those markets as the attractor,” he said.

First-home buyers armed with the new deposit scheme would be flocking to these areas, but Mr Lawless did not expect this window to remain open for long for houses, as prices rise.

He said Canberra was relatively under-represented in terms of the proportion of suburbs with a median house value under $1 million, at just 37 per cent.

“That’s the second lowest of any region around the country after Darwin,” he said.

“About 47 per cent of suburbs across Sydney have a median value below their price cap of $1.5 million.

“For first-time buyers in the ACT looking to take advantage of the deposit guarantees, the selection is going to be more limited and quite quickly we’ll see price growth just rippling into those markets and the more desirable houses surpass the price caps quite quickly.”

Exacerbating this is the lack of stock, with listings for houses 21 per cent below average for this time of year, whereas listings for units are 14 per cent above average.

All the nation’s capitals experienced rises, as demand continued to dominate supply.

But Mr Lawless said last week’s inflation shock and the dashing of hopes for further interest rate cuts had cast a shadow over the market.

“It’s not just the fact that it looks like we’re either at or approaching the bottom of the rate-cutting cycle, but also just the impact on sentiment and confidence,” Mr Lawless said.

“Cost of living pressures have bounced back. I think that in itself is probably going to dent confidence.”

If interest rates stay on hold, their potency loses impact because housing prices were rising and diluting the effect of any stronger borrowing capacity, Mr Lawless said.