Canberra’s two-tier housing market is complicating the affordability story. Photo: Michelle Kroll.

It’s become marginally easier to buy your own home in Canberra in recent years, but only because of the post-pandemic downturn after the record high prices of 2022 and the apartment boom.

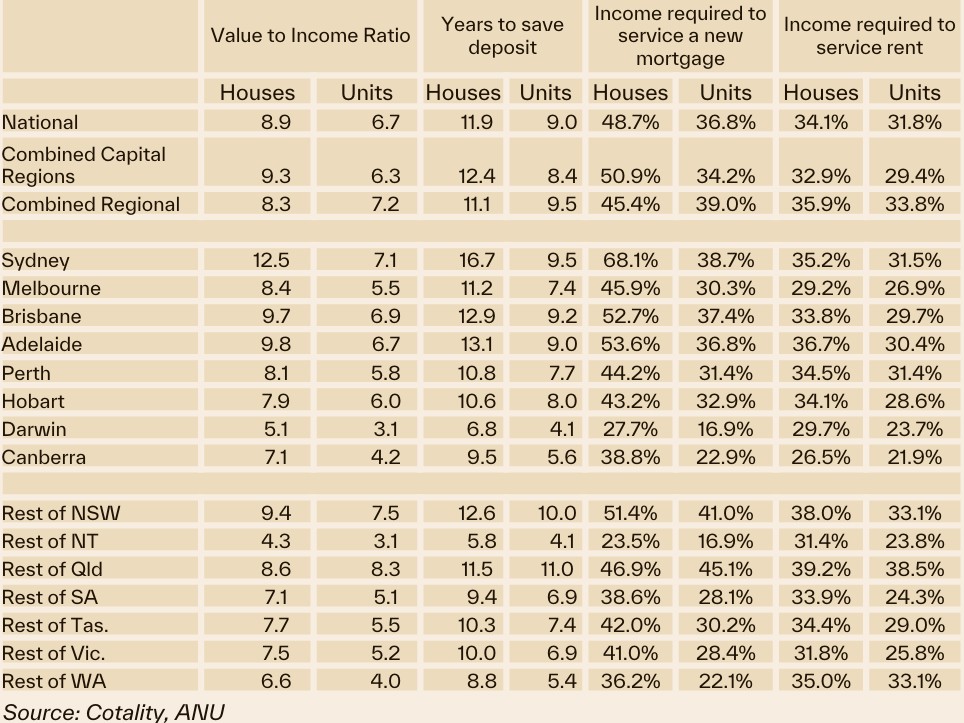

Cotality’s latest Housing Affordability Report, compiled with the ANU, shows national dwelling prices, particularly for standalone houses, continue to rise further out of the reach of many Australians and that the share of income needed to pay a mortgage has nearly doubled.

Three of the four key national indicators – the price-to-income ratio, years required to save a deposit, and the share of income needed to rent – all hit record highs in 2025, signalling that both buying and renting have reached unsustainable levels for many Australians.

Despite recent rate dips, the cost of servicing a new loan is stubbornly high, requiring 45 per cent of the median household income.

Saving a standard 20 per cent deposit nationally takes nearly 12 years, and now over a decade in four major capital cities, Sydney, Adelaide, Brisbane, and Perth.

Affordability has deteriorated most sharply for houses. The median house value is now 8.9 times the average income, up from 6.6 five years ago, and it takes almost 12 years to save a deposit, 34.6 per cent longer than five years ago.

Things are only marginally better in Canberra, where it takes 9.5 years to save a deposit for a house and 38.8 per cent of household income to service the mortgage. In 2020, it was just 25 per cent.

The median house value is 7.1 times the median income, down from 7.7 in September 2022.

Overall, the median dwelling value is 6.2 times the median income, down from 6.8; it takes 8.2 years to save a deposit, and the mortgage repayments chew up about a third of household income (33.5%).

The data shows the two-tier nature of the Canberra market, with the median unit value 4.2 times the median income, requiring 5.6 years to save a deposit and needing 22.9 per cent of income to service the mortgage.

The oversupply of much cheaper units and the ACT’s higher incomes are skewing the Canberra data, but in a market again on the rise due to interest rate cuts and the Commonwealth’s first home buyer changes, affordability is likely to worsen in the long term.

Housing affordability metrics by house and unit, September 2025

While the first home buyer changes – a 5 per cent deposit and no lenders mortgage insurance – will reduce saving times, borrowers will still have to be able to service the mortgage.

Most industry commentators say the scheme will peter out as property values, particularly for houses, are driven up to reach or exceed the $1 million cap in Canberra.

Cotality Head of Research, Eliza Owen, said over the year to date, Canberra values had risen 3.3 per cent.

“What this data tells us is that a housing market downturn is not a sustainable solution to housing affordability, because we get to a point where supply or falling home values is basically a signal to the market to restrict supply,” she said.

Ms Owen said the market could again stall next year due to rising inflation, which could change the interest rate trajectory, but that was not a solution to housing affordability, just part of the market cycle.

“If you want real, lasting structural change that has to come from things like tax reform, changes to housing supply and [buyer] incentives,” she said.

Ms Owen indicated that, with the current stock in Canberra, house prices were unlikely to moderate enough to become more affordable.

She said there had been an average of 67 house approvals a month over the past six months, well below the decade-average of 95 houses a month.

“So from the dwelling approvals data, it looks like there is that restriction of supply happening,” Ms Owen said.

“The fact that you have a median house value of over a million dollars, the fact that the housing affordability metrics for Canberra houses are quite high, that probably tells you that no, there’s not enough [stock] to make houses comfortably affordable.”

Ms Owen said the affordability impacts were being seen higher up the income ladder, and that there were many adverse consequences from a lack of adequate, affordable housing.

She said some would look to higher-density housing, cities could lose their young people to the regions or overseas, and more pressure would come on the bank of mum and dad or inheritances, reinforcing the wealth gap and the haves and the have-nots of property ownership.

“You have people who get stuck in the rental market, which can also have consequences for people later in life if they’re retired and they still have rental costs,” Ms Owen said.

The numbers would only worsen without meaningful reform on both the supply and demand side, she said.

Canberra’s rental affordability is actually better than the other capitals, with 26.5 per cent of income required to pay house rent, and 21.9 per cent for a unit.

But the 11th annual National Shelter-SGS Economics and Planning Rental Affordability Index shows that Canberra’s high incomes mask the situation for those on low and fixed incomes.

The index found that people receiving JobSeeker and pensioners face ‘Severely’ to ‘Critically’ unaffordable rents in the ACT.

A hospitality worker would need to spend 40 per cent of their income on rent, while a minimum-wage couple faces a rent burden of 31 per cent of their combined income, placing both households in rental stress.